Sign-up to receive Newmark Industrial Thought Leadership updates.

- Insights>

- Market Report Page>

- U.S. Industrial Market: Conditions & Trends

U.S. Industrial Market: Conditions & Trends

May 16, 2024

Newmark presents the first quarter 2024 U.S. Industrial Market: Conditions & Trends report.

Introduction

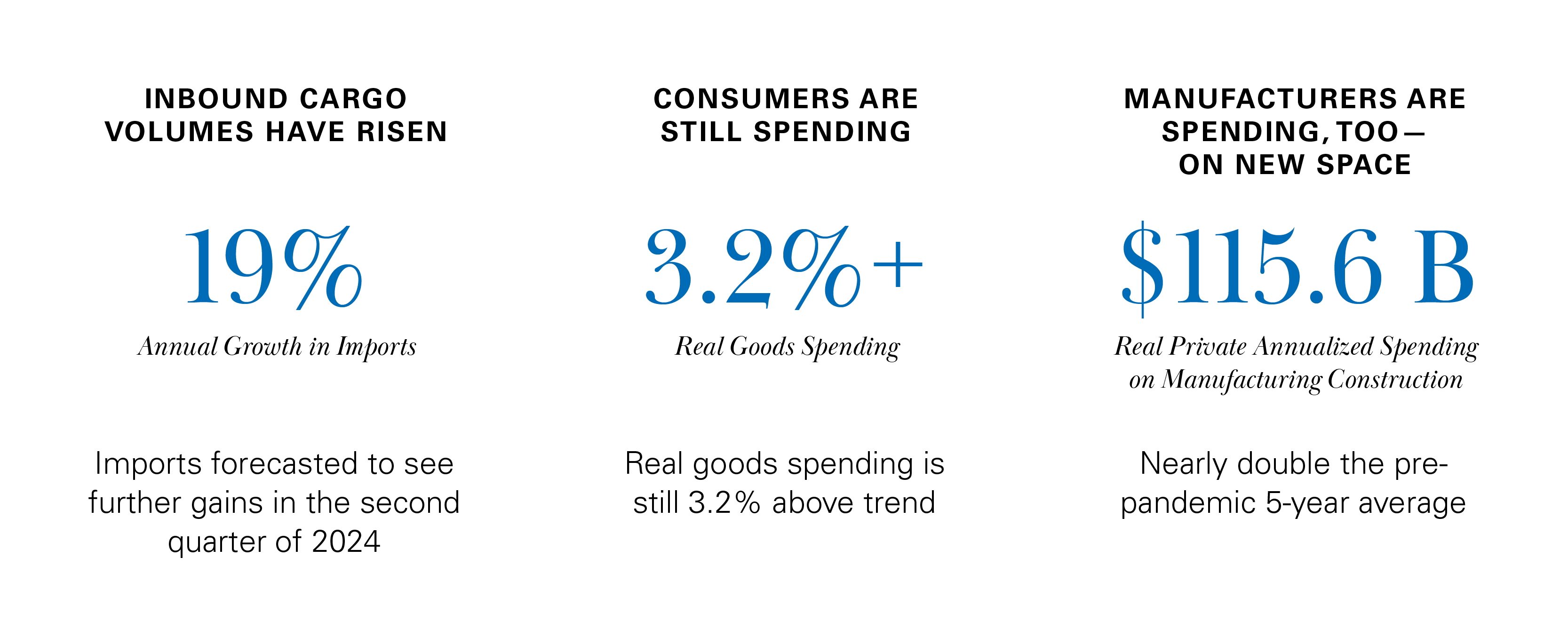

In the past two years, one billion square feet of new industrial space has delivered in the U.S., a tally that historically took four years to reach. Supply headwinds are leading to rising vacancies amid softer demand, but the impact varies by market and property segment.

To read the report, please download the PDF.

Economic Conditions and Demand Drivers

- Inflation remains above the target rate of 2.0%. With the job market largely sound, the first Fed rate cut will be prolonged. At the end of 2023, the market expected the first rate cut to come in the first half of 2024; at the end of the first quarter of 2024, that expectation has moved to September. That, too, may still be optimistic.

- Evolving trends and new players in e-commerce are driving a comeback in leasing; e-commerce accounted for 14.7% of first quarter 2024 top leasing activity up from 3.5% one year ago.

- Manufacturing construction spending has surged. In the last 12 months, $108 billion in manufacturing construction flowed into Southern states, nearly as much as the rest of the country combined.

Leasing Market Fundamentals

- Nationally, absorption measured 27.9 msf in the first quarter of 2024, the softest quarter of net absorption since 2011, but a demonstration of the market’s resilient demand. Secondary and tertiary markets absorbed 92% of that absorption.

- Vacancy continues to increase as new supply puts pressure on fundamentals. Vacancy rose to 6.0% in the first quarter of 2024, on the heels of 108 msf in new deliveries. Mirroring the national trend, all but one industrial market (Broward County, Florida) experienced increased vacancy year over year.

- Asking rent growth continues to decelerate, measuring 7.2% annually and essentially flat quarter over quarter. Rents, particularly in big-box space, will likely see a modest reset this year.

Capital Markets

- The first three months of the year ushered in $16.9 billion in sales volume and the seventh consecutive quarter of annualized declines. With the capital markets anticipating at least one interest rate cut to come this year – and growing sentiment that 2024 will be a good ‘vintage’ – volumes are likely to increase in coming quarters.

- Private – and public-market industrial cap rates continue an adjustment process in the face of financial market volatility. Average private-market cap rates expanded 10 bps from the end of last year to 5.5%.

- Overall, CRE debt origination remained relatively flat in 1Q24 – except for industrial, which roared back with 49% growth year over year, underlining a positive outlook for improving market fundamentals.

Outlook

- Vacancy will increase further as supply will likely outpace demand throughout the balance of the year. Supply – both in deliveries, and in development – will fall back to pre-pandemic levels by 2025.

- With normalizing demand, industrial staffing has been flat. However, evolving labor dynamics stand to impact the industrial market. Potential strikes threaten East Coast port and transcontinental rail activity, while labor organization may spread across the Southern manufacturing sector. Looking ahead, hundreds of thousands of jobs are needed in coming years to support booming manufacturing construction underway.

- Record industrial loan maturities are coming due in 2024. However, among all property types, the industrial sector has the lowest share of potentially troubled loans maturing.